26th April 2021

When you have $1 to invest, how do you consider veering away from the tried and tested index? In this blog we’re going to compare returns from Apple to the S&P 500 index. We’re going to look at performance over 1, 5 year periods and then since IPO of Apple.

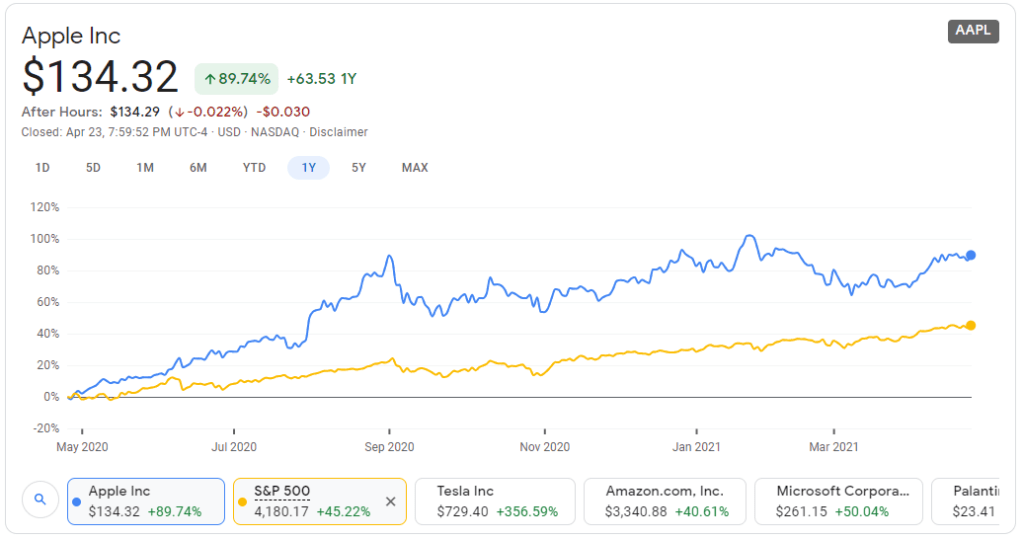

1 year comparison of Apple vs S&P 500 Index (as of 26th April 2021)

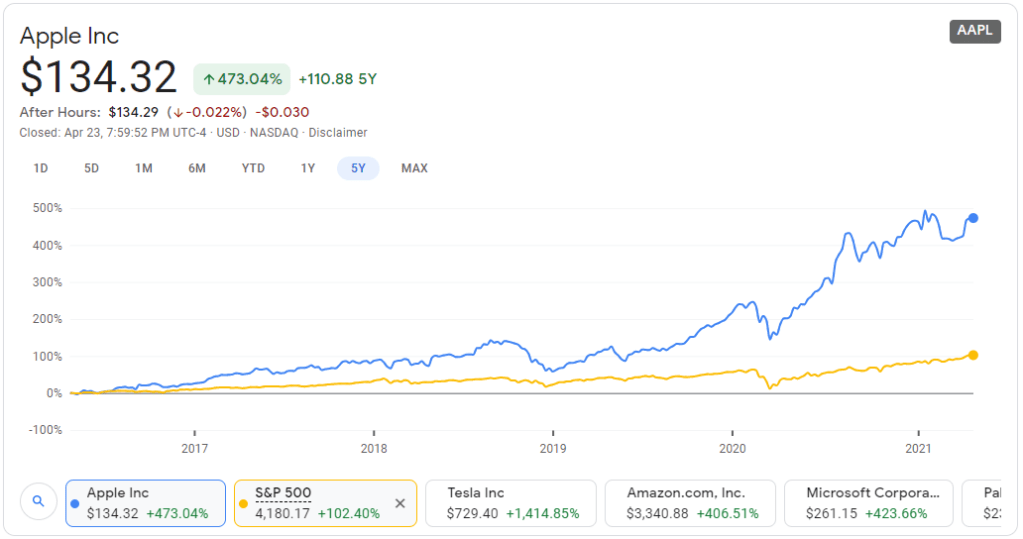

5 year comparison of Apple vs S&P 500 Index (as of 26th April 2021)

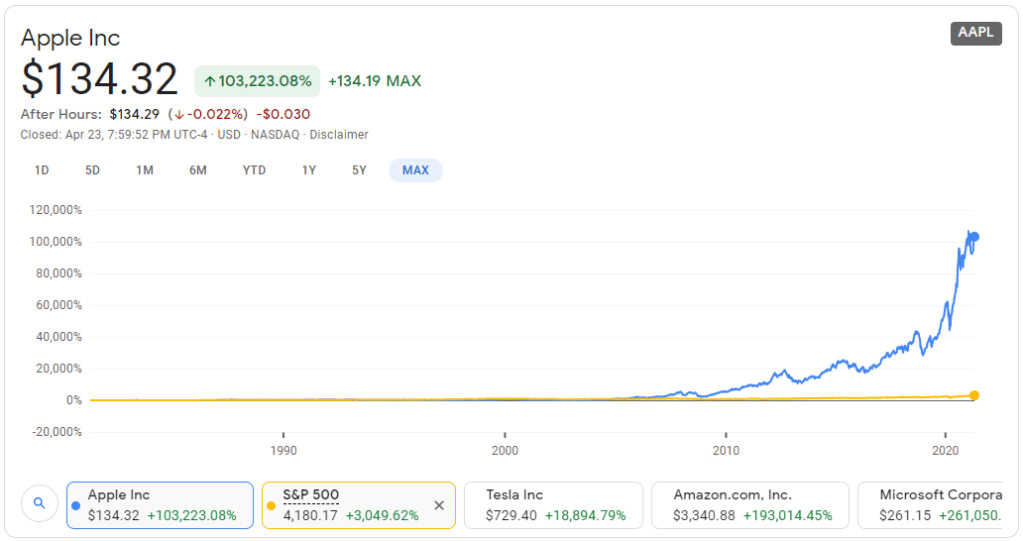

Apple, Max time span, vs S&P 500 Index (as of 26th April 2021)

As you can clearly see, Apple wins out over the index on every occasion. So how do the major financial ratios compare when assessing the 2;

Assessment of Apple –

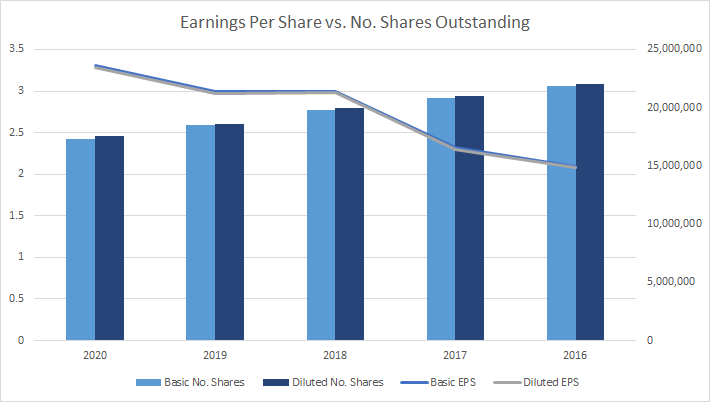

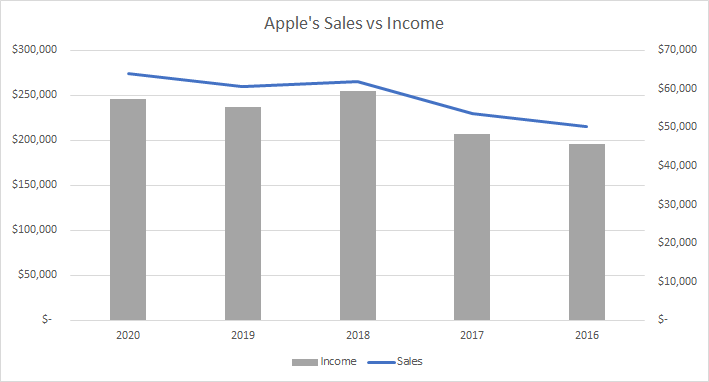

Apple clearly has a structured share buy back plan in place compared to the relatively flat earnings.

As such over the past 5 years Apple’s bucket of distributable Income has increased by circa 26% and at the same time the Number of Shares available has decreased by circa 20%. As such if you were a shareholder for the full 5 years you would have received about 58% of distributable Income growth across that period (i.e. 126%/80%). That equates to about 9% per annum compound interest Income growth.

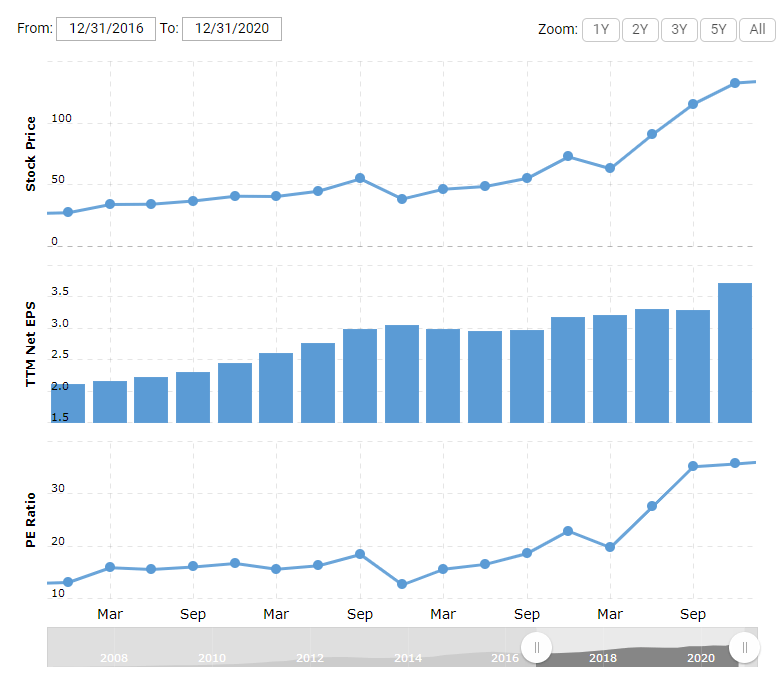

In the meantime the Apple share price rose from $28.95 at the beginning of 2017 to $133.72 at the end of 2020 – circa 462% increase.

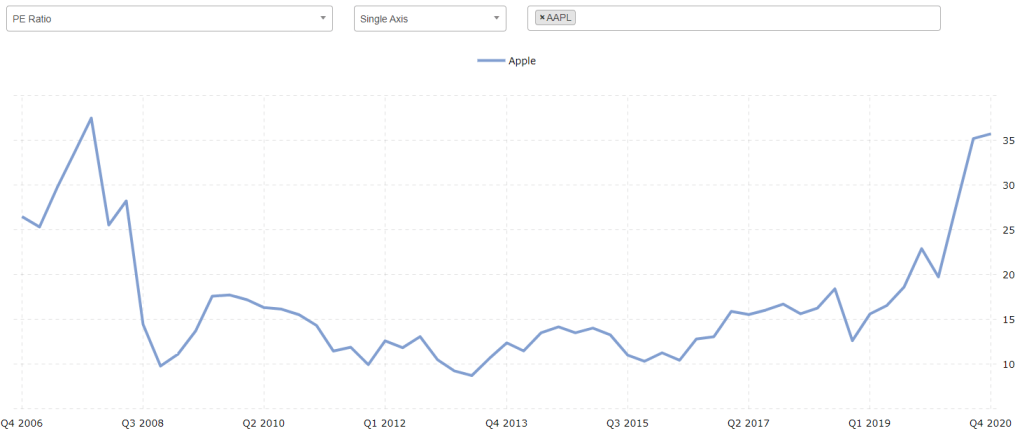

Therefore while we’ve seen a large spike in the share price, it has currently outpaced the earnings leading to a higher Price to Earnings ratio (or P/E ratio). The last time Apple had a P/E ratio at this level was in late 2007 just before the Global Financial Crisis.

The below graph shows the PE spike prior to the GFC and the current PE. Based on this information we can start to see that the market is currently placing a lot more future value on Apple compared to the past 12 years. But what’s changed?!

Let’s compare the S&P500 Index’s fundamentals.

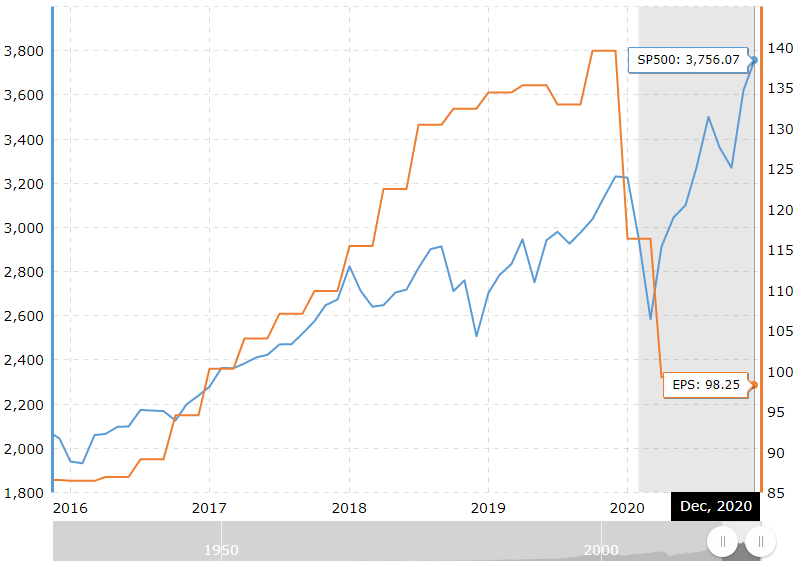

Since COVID-19 hit, we’ve seen a hard hit to earnings. This has meant that whilst earnings have dropped off a cliff, the S&P 500 has continued to rise causing a large gap between Price and Earnings. Overtime we can always expect a ‘reversion to the mean’ and at this point to quote the great man Benjamin Graham, in the short term the stock market is a voting machine and in the long term it is a weighing machine.

Whilst it’s true that Earnings have been hit, the market is basically temporarily turning a blind eye to the dip. As such if the earnings dip in the S&P500 continues then we’ll start to see pressure on prices.

Summary:

- Apple has outperformed the S&P500 over all time frames; 1 year, 5 years and over the long term

- Earnings during COVID times have been stable growth for Apple and have hit the S&P500 hard.

- The market has pushed Apple’s share price up over 400% in capital value in the past 5 years, whereas a similar investment in the S&P500 would have only increased a tad over 80%.

- Apple has a structured buy back program in place whereas the S&P 500 is dependent upon all entities deciding on buy backs.

- Apple has a much higher level of market risk compared to the S&P 500 (1 business vs 500 businesses), however for the higher level of risk there is a potential for higher return over the long term.

- Generally both Apple and the S&P 500 are trading a multiples much higher than their historical average Price to Earnings ratio. Caution!

- When you’re looking at 1 company as an investment always ask yourself – will these products (and any future products they have in the pipeline) continue to sell as well as they are selling right now. If you invest in a single company there’s always a risk it’s products may go off the boil – whereas the S&P500 always adjusts for the largest 500 companies in the US.